Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Question: “What’s the Real Story Behind 50-Year Mortgages — Smart Opportunity or Long-Term Trap?” 🏡⏳

Answer:

If you’ve been following real estate news lately, you’ve probably seen the buzz: 50-year mortgages. Some people love the idea, some are terrified, and most are wondering whether it’s genius… or a debt sentence.

Hi!, I’m Chad Ziemke with Century 21 Atwood, let’s break it down so you can make the right move without the hype.

⭐ What Is a 50-Year Mortgage?

A 50-year mortgage simply stretches your loan payoff period to 600 months instead of 360. The idea is straightforward:

👉 Longer term = Lower monthly payment.

👉 Lower monthly payment = More buying power.

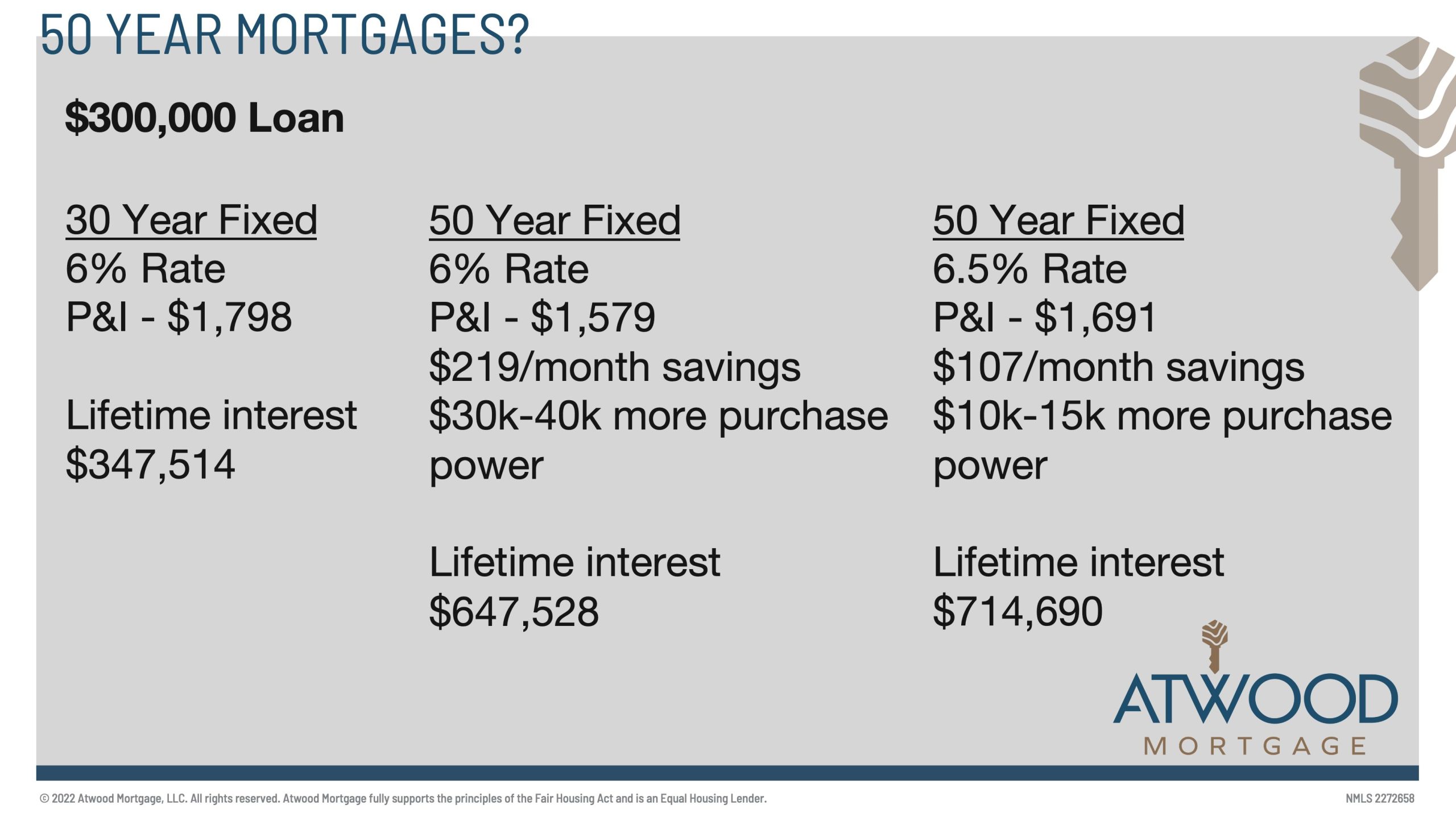

Using a example by Atwood Mortgage: (Graphic above)

-

30-Year Fixed at 6%

P&I: $1,798

Lifetime interest: $347,514 -

50-Year Fixed at 6%

P&I: $1,579

Payment savings: $219/month

Lifetime interest: $647,528

Yep… lower payment, but at a huge long-term cost.

⭐ The Opportunity (Where It Could Make Sense)

Let’s be fair — 50-year mortgages aren’t all bad. The main benefits:

✔️ Lower monthly payment

This can free up cash flow, especially for first-time buyers or households trying to balance child-care, inflation, student loans, etc.

✔️ Increased purchase power

Buyer may qualify for more home simply because the payment is stretched over more years.

✔️ Flexibility

Some borrowers simply want breathing room in their budget. A 50-year loan lets them do that.

⭐ The Drawbacks (The Part Most People Skip Over)

Let’s talk about the math — because it’s eye-opening:

⚠️ You pay significantly more interest

Almost double in many cases. That’s not a typo.

⚠️ You build equity VERY slowly

Equity = wealth.

A slow equity-build means slower wealth-building.

⚠️ You’re still paying a mortgage into your 70s or 80s

This can interfere with retirement planning or financial independence.

⚠️ It may encourage buyers to stretch too far

Just because you can buy more house… doesn’t mean you should.

⭐ Dave Ramsey’s Take (Spoiler: He Hates It 🙃)

Dave Ramsey has been crystal clear on mortgages for years. His recommendation:

“The only kind of mortgage I recommend is a 15-year, fixed-rate loan where the payment is no more than 25% of your monthly take-home pay.”

Source: Dave Ramsey on Facebook

https://www.facebook.com/daveramsey/posts/the-only-kind-of-mortgage-i-recommend-is-a-15-year-fixed-rate-loan-where-the-pay/1067686291387651/?utm_source=chatgpt.com

Ramsey’s philosophy:

Shorter term = less interest = faster wealth building.

Whether you agree with him or not, the math is hard to argue with.

⭐ So, Should You Consider a 50-Year Mortgage?

It depends!

A 50-year mortgage might make sense if:

-

You need the lowest monthly payment possible

-

You plan to refinance later

-

You’re buying a starter home

-

You’re optimizing monthly cash flow, not long-term interest cost

BUT… it may NOT make sense if:

-

You want to build equity quickly

-

You plan to retire early

-

You want to minimize interest

-

You’re purchasing a long-term residence

As always — your long-term goals matter more than any trend.

⭐ Bottom Line

A 50-year mortgage can offer short-term relief and more buying power… but often at the expense of long-term wealth. Before you jump in, it’s wise to look at the numbers, compare options, and make sure the loan truly fits your financial path.

If you’re thinking about your next move or want to compare mortgage options with real numbers, I’m here to help.

I’m Chad Ziemke with Century 21 Atwood and Atwood Mortgage— and my goal is to help you make the smartest move, not just the easiest one. 💛🏡